You're between jobs. Or maybe you're a recent grad waiting for that "real" corporate benefits package to kick in. You need a bridge. Naturally, you look at UPMC because, well, they own half the hospitals in Pennsylvania. But here is the thing: if you go looking for "UPMC short term health insurance," you are going to hit a wall.

Why? Because UPMC Health Plan doesn't actually sell short-term medical plans.

They just don't. It’s a common point of confusion. People assume a giant like UPMC would have a "quick fix" plan for a 30-day gap, but they’ve basically staked their reputation on ACA-compliant, comprehensive coverage. If you want a plan that lasts three months and costs $80, you’re looking in the wrong place. But before you close this tab, you should probably understand why they don't offer it—and why that might actually be a good thing for your bank account.

The Reality of Temporary Coverage in Pennsylvania

Pennsylvania insurance laws are kind of intense. As of 2026, the state still keeps a tight leash on short-term limited-duration insurance (STLDI). We're talking about a cap of three months for the initial term, with maybe a one-month renewal.

Basically, the state doesn't want people using these as permanent insurance.

UPMC focuses on "Major Medical." These are the "real" plans. They cover the stuff short-term plans usually laugh at, like maternity care, mental health, and those wildly expensive prescriptions. When you see someone searching for UPMC short term health insurance, what they usually need is a Special Enrollment Period (SEP) or a specific low-cost ACA plan, not a "junk" policy that won't cover them if they trip on a curb and need an MRI.

Why UPMC Skips the Short-Term Market

Honestly, short-term plans are a gamble for the insurer and the patient. UPMC is a "provider-payer" model. They own the doctors. They don't want you showing up at UPMC Presbyterian with a short-term plan from some random out-of-state company that refuses to pay for your gallbladder surgery because of a "pre-existing condition."

They’d rather get you on a plan like UPMC First Care.

This is their answer to the "I need something cheap and fast" crowd. It isn't "short-term" in the legal sense, but it's designed to be accessible. You get $0 copays for your first primary care visit and your first specialist visit. It feels like a bridge, but it’s actually a full-sized bridge that won't collapse under you.

The "Bridge" Alternatives You Actually Need

If you were dead set on finding UPMC short term health insurance because you’re in a transition, you have better options. You've got to look at the "Qualifying Life Events."

- Lost your job? That’s an SEP.

- Moved to PA from another state? SEP.

- Turned 26 and got booted from the parents' plan? SEP.

You have 60 days from the event to grab a real UPMC plan. And since the "Enhanced Subsidies" from previous years are in a state of flux in 2026, you might find that a silver or bronze plan through Pennie (Pennsylvania’s exchange) is actually cheaper than a short-term plan once the tax credits kick in.

Breaking Down the Costs (Prose Style)

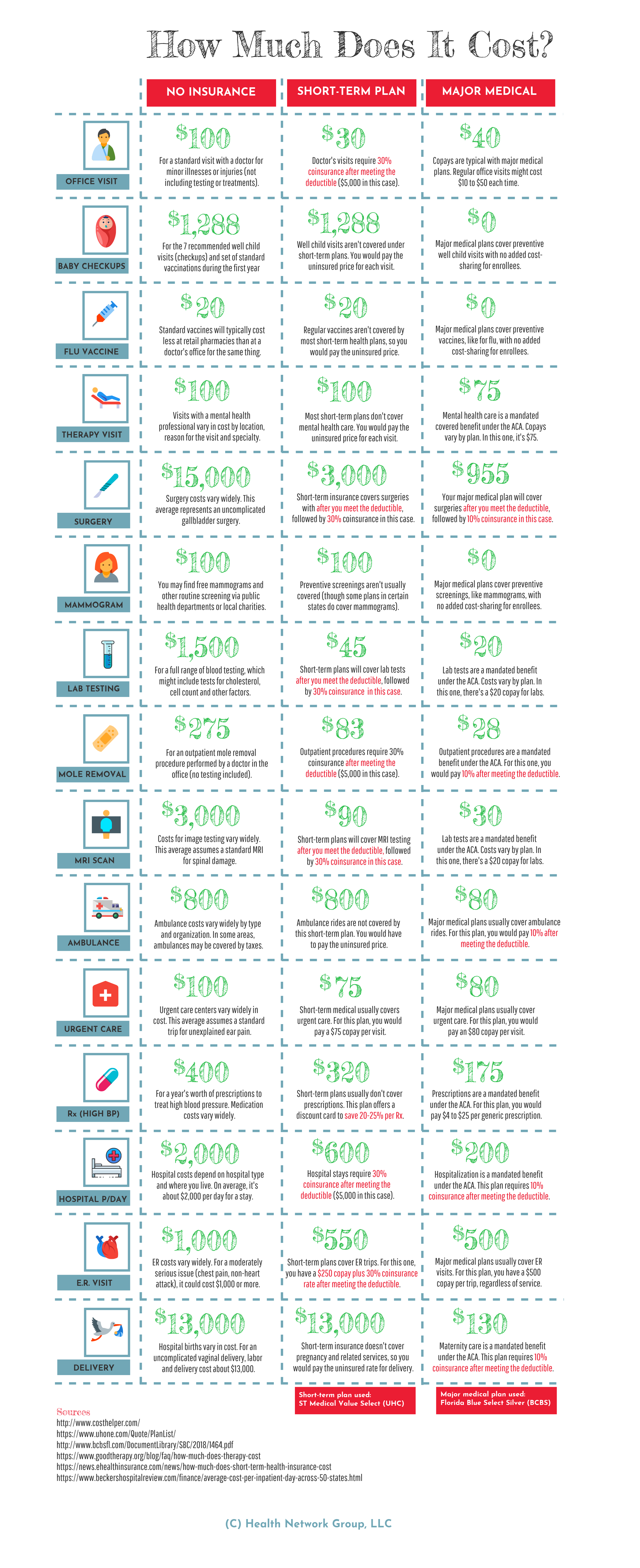

In a traditional short-term plan, you might pay a $100 premium but have a $10,000 deductible. Think about that. You're paying for the "privilege" of paying the first $10k yourself.

With a UPMC individual plan—even a high-deductible one—the math changes. You get the UPMC network. That’s huge. You aren't getting "balance billed" because the doctor is out-of-network. You get the $0 preventive care mandated by the ACA. If you’re healthy and just worried about a catastrophic accident, a Bronze-level UPMC plan via the marketplace is almost always a smarter financial move than a three-month "temporary" plan that excludes everything but the kitchen sink.

What Most People Miss About "Short-Term" Gaps

Most people think they are stuck if they miss the Open Enrollment window (which usually ends Jan 31). They think, "Well, I guess I'll just buy a short-term plan until next year."

That is a trap.

Short-term plans can deny you for pre-existing conditions. If you have asthma, or high blood pressure, or even something you didn't know you had until you filed a claim, they can just... not pay. UPMC's plans can't do that. They have to take you, regardless of your medical history, as long as you're in an enrollment window.

The Student Loophole

Are you a student at Pitt or another local school? UPMC often handles the student health plans. These aren't "short-term" insurance in the way people usually mean, but they are temporary in the sense that they cover you for the academic year. If you're looking for UPMC short term health insurance as a student, check your university's specific portal first. The 2025-2026 rates for Pitt students, for example, are often way more competitive than anything you'll find on the open market.

How to Actually Get Covered Today

Since you can't buy a literal UPMC short-term policy, here is the move you should make right now:

- Check Pennie.com. This is the only place to get the subsidies. If you're low-income or between jobs, the state might cover almost the entire premium.

- Verify your "Event." If you lost coverage in the last 60 days, you are golden. You can pick up a UPMC Health Options plan immediately.

- Look at the UPMC First Care plans. If you don't qualify for an SEP, look into "Catastrophic" plans if you're under 30. They function similarly to short-term plans (low premium, high deductible) but with much better legal protections.

Don't gamble on a fly-by-night short-term provider just because the UPMC name isn't on a "temporary" flyer. The risk of a $50,000 hospital bill because of a technicality in a short-term contract isn't worth the $40 you save on a monthly premium.

Go to the UPMC Health Plan website and look for the "Individual and Family" section. Select your county—whether you're in Allegheny, Erie, or out in Berks. The 2026 network has expanded, especially in central PA, so you might have more options than you did two years ago.

Your next move: Gather your termination of coverage letter (if you lost a job) or your tax return from last year. Head to the Pennsylvania state exchange and search specifically for UPMC plans. If you're outside the enrollment window and don't have a qualifying event, call a local broker to see if you qualify for Medicaid (UPMC for You), which allows for year-round enrollment and serves as the ultimate "short-term" bridge for those who qualify financially.